Top 8 Semiconductor Companies by Revenue: Who's Really Winning the Chip Race

Revenue tells the real story of semiconductor dominance. From Samsung's memory empire to NVIDIA's AI revolution, discover the 8 largest chip companies by revenue and the diverse strategies driving their success in 2025.

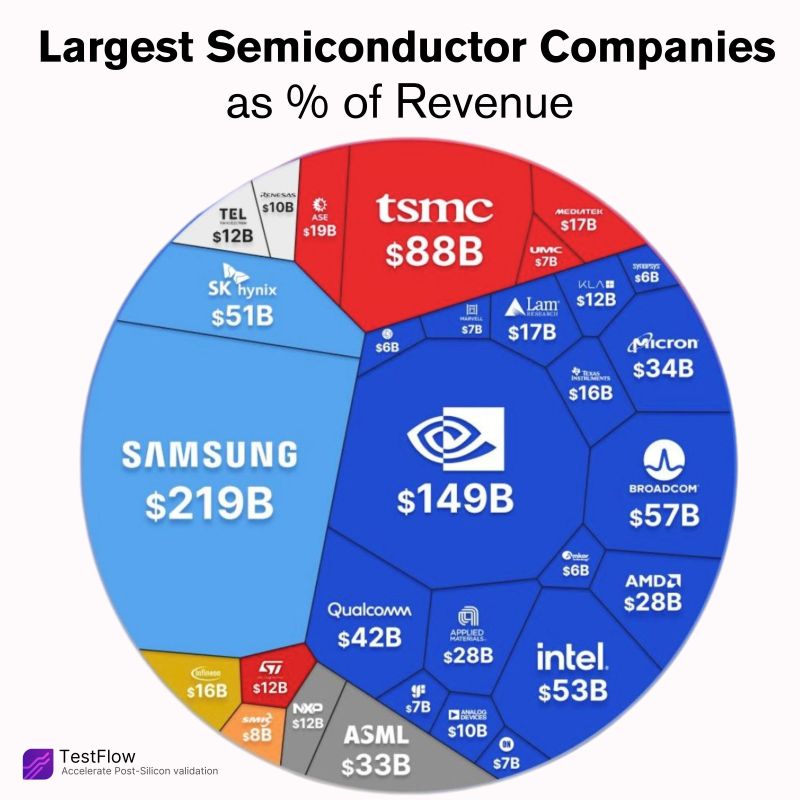

While market capitalization captures investor sentiment and future expectations, revenue reveals the true scale and current dominance of semiconductor companies. The top 8 semiconductor companies by revenue represent diverse strategies, from Samsung's memory dominance to NVIDIA's AI acceleration revolution.

These revenue leaders don't just sell chips—they shape the entire technology ecosystem. Their success stories reveal the different paths to semiconductor leadership and the strategic choices that determine who wins in the global chip race.

The Revenue Champions

2024 Revenue Rankings

Samsung

Memory & Logic Leader

NVIDIA

AI & GPU Powerhouse

Samsung: The Undisputed Revenue Leader

$219B: How Samsung Dominates

Samsung's semiconductor revenue leadership stems from its unique position as both a memory giant and a logic competitor, combined with massive vertical integration across the entire technology stack.

Memory Dominance

- • 45% of global DRAM market

- • 35% of global NAND flash market

- • Leading HBM supplier for AI

- • Automotive memory growth

Logic & Foundry

- • Exynos mobile processors

- • Advanced foundry services

- • 3nm process technology

- • Custom silicon for hyperscalers

Vertical Integration

- • Smartphone integration

- • Display and semiconductor synergy

- • Internal consumption benefits

- • Technology transfer advantages

Revenue Breakdown

By Product Category

- • Memory (DRAM + NAND): ~$140B (64%)

- • System LSI: ~$45B (21%)

- • Foundry Services: ~$20B (9%)

- • Other semiconductors: ~$14B (6%)

Strategic Advantages

- • Massive R&D investment ($22B annually)

- • Leading-edge manufacturing

- • Diversified customer base

- • Technology leadership in memory

NVIDIA: Riding the AI Wave to $149B

From Gaming to AI Dominance

NVIDIA's transformation from a gaming GPU company to the leader of the AI revolution represents one of the most successful pivots in semiconductor history. Their revenue growth has been nothing short of extraordinary.

Revenue Growth Story

AI Market Drivers

- • ChatGPT and LLM training demand

- • Data center AI acceleration

- • Cloud provider GPU adoption

- • Enterprise AI inference needs

- • Autonomous vehicle development

- • Scientific computing applications

Product Portfolio Success

Data Center

H100, A100 GPUs

Gaming

GeForce RTX series

Professional

Automotive, Omniverse

The Manufacturing and Infrastructure Leaders

TSMC - $88B

The World's Most Advanced Foundry

Market Position

- • 62% of global foundry market share

- • 92% of advanced node production

- • Exclusive 3nm mass production

- • Apple, NVIDIA, AMD dependency

Technology Leadership

- • Leading EUV lithography adoption

- • 2nm development on track

- • Advanced packaging capabilities

- • Highest manufacturing yields

Broadcom - $57B

The Silent Infrastructure Giant

Product Portfolio

- • WiFi and Bluetooth chips

- • Networking ASICs and switches

- • Storage controllers and adapters

- • RF front-end modules

Market Strategy

- • Apple partnership (wireless chips)

- • Enterprise networking dominance

- • Consistent high margins

- • Strategic acquisitions

Intel - $53B

The Comeback Story

Challenges

- • Lost manufacturing leadership

- • Market share decline in CPUs

- • Mobile market failure

- • Competition from AMD, ARM

Turnaround Strategy

- • Intel Foundry Services expansion

- • AI accelerator development

- • Advanced packaging focus

- • Government support (CHIPS Act)

The Memory Specialists

SK Hynix

Market Position

- • #2 in global DRAM market (28%)

- • #6 in NAND flash market

- • Leading HBM memory supplier

- • AI infrastructure enabler

Growth Drivers

- • AI training memory demand

- • Data center expansion

- • 5G infrastructure growth

- • Automotive memory adoption

Micron

Market Focus

- • #3 in global DRAM market (23%)

- • #4 in NAND flash market

- • Strong in enterprise storage

- • Automotive memory growth

Differentiation

- • Advanced 3D NAND technology

- • US-based manufacturing

- • Strong hyperscaler relationships

- • Emerging memory technologies

Qualcomm: The Mobile Chip Leader ($42B)

Snapdragon Ecosystem Dominance

Qualcomm's revenue leadership in mobile semiconductors stems from its comprehensive system-on-chip approach, combining processors, modems, RF, and AI capabilities in integrated solutions.

Mobile Dominance

- • 40%+ Android SoC market share

- • Premium smartphone focus

- • 5G modem leadership

- • RF front-end integration

Diversification

- • Automotive processors growing

- • IoT and edge AI expansion

- • PC processor entry (ARM)

- • XR/VR platform development

Technology Edge

- • Leading 5G implementations

- • AI engine optimization

- • Advanced camera ISPs

- • Power efficiency focus

Revenue Diversification Strategy

Current Revenue Mix

- • Handsets: ~$24B (57%)

- • RF Front End: ~$8B (19%)

- • Automotive: ~$5B (12%)

- • IoT: ~$5B (12%)

Growth Opportunities

- • Automotive ADAS and infotainment

- • Edge AI and industrial IoT

- • PC and laptop processors

- • Extended reality platforms

Revenue Analysis and Market Trends

Market Concentration Analysis

Revenue Distribution

Growth Drivers

- • AI and machine learning acceleration

- • Data center expansion

- • 5G infrastructure deployment

- • Automotive electrification

- • Edge computing growth

2025-2030 Projections

Total semiconductor market by 2030

Expected CAGR 2025-2030

Growth primarily driven by AI

Revenue Reveals the Real Winners

The revenue rankings of semiconductor companies tell a story of diverse strategies and market positioning. Samsung's memory dominance, NVIDIA's AI revolution, and TSMC's manufacturing excellence each represent different paths to semiconductor leadership.

What's remarkable is how these companies have carved out distinct competitive moats: Samsung through vertical integration and memory leadership, NVIDIA through AI acceleration dominance, TSMC through advanced manufacturing capabilities, and Qualcomm through mobile ecosystem control.

Looking ahead, revenue growth will increasingly be driven by AI applications, edge computing, and automotive electronics. The companies that successfully adapt their strategies to these emerging markets while maintaining their core strengths will define the next chapter of semiconductor leadership.

Validate Chips from Any Vendor

Whether your chips come from Samsung, NVIDIA, TSMC, or any other semiconductor leader, comprehensive validation ensures optimal performance and reliability. TestFlow's platform supports testing across all major chip architectures and vendors.