Top 5 Semiconductor Foundries by Market Share: The Manufacturing Powerhouses

It's not just about design—most chips are made by foundries. Discover the specialized factories that manufacture semiconductors for the world's biggest tech companies and how TSMC's 62% dominance shapes the entire industry.

Behind every smartphone processor, AI accelerator, and automotive chip lies a sophisticated manufacturing ecosystem. While design companies like NVIDIA and Qualcomm capture headlines, it's the foundries—specialized chip manufacturing facilities—that transform silicon wafers into the processors powering our digital world.

The foundry business represents one of the most capital-intensive and technologically demanding industries on Earth. With individual facilities costing $20+ billion and requiring years to build, only a handful of companies can compete at the leading edge. Let's explore the top 5 foundries that manufacture the majority of the world's semiconductors.

Global Foundry Market Share Breakdown

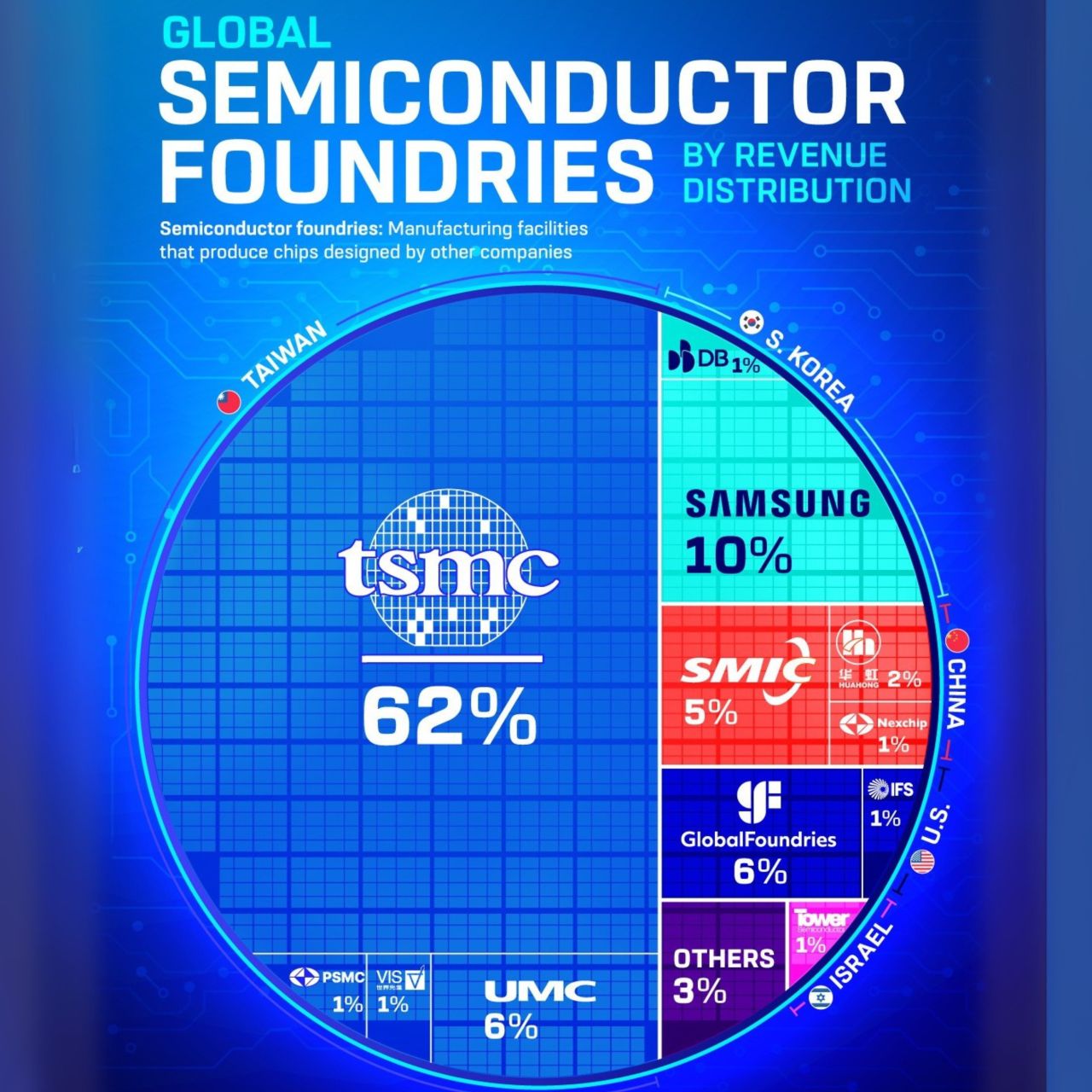

2024 Foundry Revenue Rankings

TSMC

Taiwan Semiconductor Manufacturing Company

The undisputed king of foundries. TSMC dominates advanced chip manufacturing, powering nearly every major AI, smartphone, and data center chip today.

Samsung

Memory + Foundry Hybrid

GlobalFoundries

Mature Node Specialist

UMC

Legacy Technology Focus

SMIC

China's Foundry Champion

Market Concentration

TSMC's market dominance

Top 5 foundries combined share

Total foundry market size (2024)

TSMC: The Foundry King ($54.2B Revenue)

Unmatched Technology Leadership

TSMC's foundry model revolutionized the semiconductor industry, enabling fabless companies to access world-class manufacturing without massive capital investment. Today, TSMC manufactures chips for over 500 customers worldwide.

Technology Nodes

- • 3nm: Mass production leader

- • 5nm: High-volume manufacturing

- • 7nm: Mature, high-yield process

- • 2nm: Development on track

Key Customers

- • Apple: 23% of revenue

- • Qualcomm: 8.9% of revenue

- • AMD: 7.6% of revenue

- • NVIDIA: 6.3% of revenue

Competitive Moat

- • 2-3 generation lead

- • Highest manufacturing yields

- • Massive R&D investment

- • Customer co-development

TSMC's Strategic Advantages

Pure-Play Model

- • No competition with customers

- • Focus purely on manufacturing excellence

- • Shared R&D costs across customers

- • Technology-agnostic approach

Execution Excellence

- • Consistent technology roadmap delivery

- • Industry-leading yields and quality

- • Scalable manufacturing capacity

- • Strong customer partnerships

The Competition: Strategies and Specializations

Samsung Foundry: The Hybrid Approach

Competitive Position

- • Only other leading-edge competitor

- • 3nm process in production

- • Gate-All-Around (GAA) technology

- • Strong in memory integration

Challenges

- • Customer trust issues (yield concerns)

- • Competition with own System LSI division

- • Lower market share despite capabilities

- • Need to prove foundry commitment

GlobalFoundries: The Mature Node Leader

Strategic Focus

- • Stopped advanced node development (7nm+)

- • Focus on 22nm, 28nm, and older

- • Automotive and IoT specialization

- • RF and analog process expertise

Market Advantages

- • Lower costs for mature applications

- • Stable, proven processes

- • Geographic diversification

- • Strong automotive relationships

UMC

Specialization

- • 28nm and older technologies

- • Specialty process variants

- • Embedded memory solutions

- • Cost-competitive manufacturing

SMIC

Growth Strategy

- • China's largest foundry

- • Rapid capacity expansion

- • 14nm process capabilities

- • Government support backing

Technology Node Competition

Leading-Edge vs. Mature Nodes

The foundry market is bifurcated between leading-edge nodes (7nm and below) where only TSMC and Samsung compete, and mature nodes (28nm and above) where multiple players serve different market segments.

| Process Node | TSMC | Samsung | Others | Applications |

|---|---|---|---|---|

| 3nm | ✓ Mass Production | ✓ Limited Production | — | iPhone 15 Pro, M3 |

| 5nm | ✓ High Volume | ✓ Production | — | A15/A16, M1/M2, Snapdragon |

| 7nm | ✓ Mature | ✓ Available | — | AMD Ryzen, NVIDIA RTX |

| 14nm | ✓ | ✓ | SMIC | Mid-range mobile, automotive |

| 28nm+ | ✓ | ✓ | GF, UMC, SMIC | IoT, automotive, industrial |

The Economics of Process Nodes

Leading-Edge Economics

- • 3nm wafer: ~$20,000 each

- • High margins but limited customers

- • Requires massive volumes to justify

- • Technology co-development needed

Mature Node Economics

- • 28nm wafer: ~$1,000 each

- • Lower margins but broader market

- • Stable, predictable demand

- • Multiple competitive suppliers

Foundry Market Dynamics and Future Trends

Capacity and Investment Trends

Capacity Expansion

- • TSMC: $40B annual capex (2024-2026)

- • Samsung: $25B foundry investment

- • Intel IFS: $20B fab construction

- • SMIC: Rapid domestic expansion

Geographic Diversification

- • TSMC Arizona fabs (4nm, 3nm)

- • Samsung Texas facility expansion

- • Intel Ohio mega-site development

- • European foundry initiatives

Emerging Foundry Players

Intel IFS

Leveraging internal capabilities for external customers

Tower Semiconductor

Analog and mixed-signal specialty foundry

X-FAB

Automotive and industrial focus

Future Market Projections

Foundry market size by 2030

Expected annual growth rate

TSMC's likely market share

Foundry Validation and Quality Assurance

Manufacturing Quality Control

Foundries must maintain exceptional quality across diverse customer designs, process technologies, and volume requirements. This demands sophisticated validation and quality control systems.

Critical Quality Metrics

- • Wafer-level yield optimization

- • Process variation control

- • Defect density minimization

- • Parametric test correlation

- • Reliability qualification

- • Customer-specific requirements

Advanced Monitoring

- • Real-time process monitoring

- • AI-driven yield prediction

- • Statistical process control

- • Inline metrology systems

- • Predictive maintenance

- • Customer feedback integration

TestFlow for Foundry Validation

Foundries and their customers need comprehensive validation to ensure manufactured chips meet all specifications. TestFlow's AI-powered platform provides foundry-grade testing capabilities, helping verify that silicon performs exactly as designed across all operating conditions.

Learn About Foundry TestingThe Foundry Ecosystem Shapes Technology

The foundry business isn't just competitive—it's strategic. These manufacturing powerhouses don't just make chips; they enable entire industries and determine what's technologically possible. TSMC's dominance with over 60% market share means that a single company in Taiwan controls the production of the world's most advanced semiconductors.

The concentration of advanced manufacturing capabilities in so few hands creates both opportunities and risks. While it enables incredible technological progress and economies of scale, it also creates supply chain vulnerabilities that governments and companies are actively working to address through geographic diversification and capacity expansion.

Looking ahead, the foundry landscape will continue to evolve as new players enter specialized markets, existing leaders expand globally, and emerging technologies like chiplets create new manufacturing paradigms. Understanding these dynamics is crucial for anyone involved in semiconductor design, manufacturing, or supply chain management.

Validate Chips from Any Foundry

Whether your chips are manufactured by TSMC, Samsung, or other foundries, comprehensive validation ensures they meet your performance and reliability requirements. TestFlow's platform provides foundry-agnostic testing capabilities.